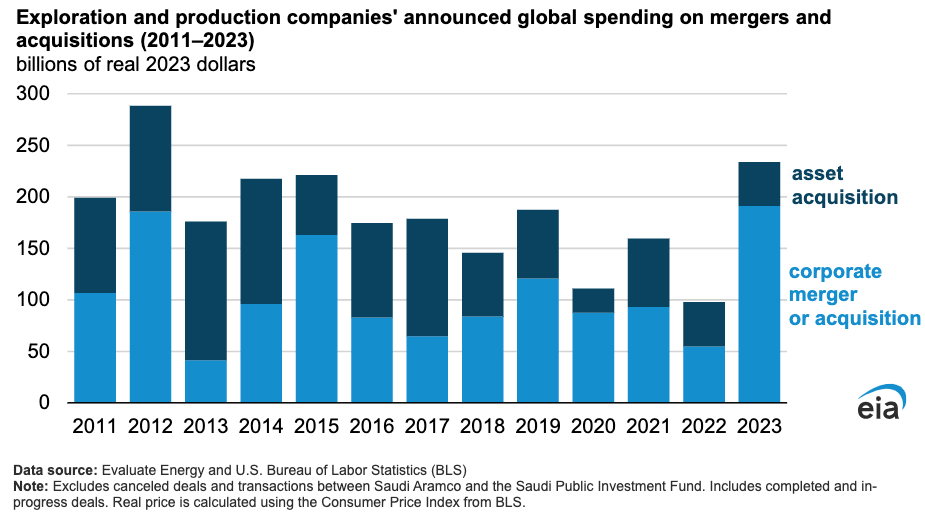

Upstream M&A Activity Hits 11-Year High

According to the Energy Information Administration (EIA) and data from the Bureau of Labor Statistics and Evaluate Energy, United States crude oil and natural gas exploration and production (E&P) companies announced US$234 billion on mergers and acquisitions (M&A) in 2023, the highest level in real 2023 dollars since 2012.

The EIA splits spending on M&A into two categories — corporate M&A and asset acquisition. Corporate M&A made up 82% of announced spending and refers to one company merging with or acquiring another company. Meanwhile, asset acquisition refers to a transfer of ownership of asset(s) to another company, such as a divestment, acreage sales, buying proved reserves, etc.

The industry has been consolidating at a rapid rate as corporate profits hit all-time highs. Buyers are looking to put excess cash to work by diversifying their asset base and increasing production, while sellers that outlasted the brutal COVID-19 pandemic-induced downturn are getting a much better price to sell. Between 2021 and the time of this writing, Hess stock increased three-fold and Pioneer Natural Resources increased more than 135%. Since the beginning of 2021, energy has been the best-performing sector in the S&P 500, producing a total return (including capital gains and dividends) of 186% compared to 49% for the index.

ExxonMobil Completes Merger With Pioneer Natural Resources

On May 3, ExxonMobil completed its US$64.5 billion acquisition of Pioneer Natural Resources. According to ExxonMobil, the merger gives the company the largest and highest-return development potential in the Permian Basin. “The combined company’s more than 1.4 million net acres [0.57 million ha] in the Delaware and Midland basins have an estimated 16 billion barrels of oil equivalent resource,” said ExxonMobil in a press release. “ExxonMobil’s Permian production volume will more than double to 1.3 million barrels of oil equivalent per day [MOEBD], based on 2023 volumes, and is expected to increase to approximately 2 MOEBD in 2027, based on initial estimates. Combining Pioneer’s differentiated Permian inventory and basin knowledge with ExxonMobil’s proprietary technologies, financial resources, and project execution excellence is expected to generate double-digit returns by recovering more resources more efficiently and with a much lower environmental impact.”

ExxonMobil has a goal to be net-zero by 2050. In an interview with Yahoo Finance in early May, Exxon Chief Executive Officer Darren Woods said the company still plans to produce fossil fuels by 2050, but it will likely make up a smaller part of the business. In the meantime, it plans to achieve net-zero Scope 1 and Scope 2 greenhouse gas emissions from its Permian unconventional operations by 2030. With the merger closed, ExxonMobil said it will leverage its Permian greenhouse gas reduction plans to accelerate Pioneer’s Scope 1 and 2 net-zero emissions goal by 15 years. ExxonMobil will apply its technologies to monitor, measure, and address fugitive methane to reduce the combined companies’ methane emissions. Using combined operating capabilities and infrastructure, ExxonMobil expects to increase the amount of recycled water used in its Permian fracturing operations to more than 90% by 2030.

Stuck In Limbo

Within weeks after ExxonMobil announced plans to buy Pioneer Natural Resources, Chevron responded in late October with its intended merger with Hess for US$60 billion, including debt. However, Chevron’s process has not been as smooth as ExxonMobil’s. The crown jewel of the deal is Hess Guyana Exploration, which has a 30% stake in the Stabroek block offshore Guyana. The other two owners of the consortium are ExxonMobil Guyana with a 45% stake and CNOOC Petroleum Guyana with a 25% interest.

ExxonMobil doesn’t want to share a slice of the Guyana pie with its closest competitor. It got CNOOC on board to block Chevron’s merger. ExxonMobil and CNOOC filed arbitration claims against Chevron in late March under grounds that they have first right of refusal to prevent a change in ownership in the Stabroek block. Regardless of the outcome, Chevron’s merger will likely take much longer to process.

| Acquirer | Acquiree | Amount |

| ExxonMobil | Pioneer Natural Resources | US$64.5 billion |

| Chevron | Hess | US$60 billion |

| Diamondback Energy | Endeavor Energy Partners | US$26 billion |

| Occidental Petroleum | CrownRock LP | US$12 billion |

| Chesapeake Energy | Southwestern Energy | US$11.5 billion |

| Chevron | PDC Energy | US$7.6 billion |

| ExxonMobil | Denbury | US$4.9 billion |

| APA | Callon Petroleum Company | US$4.5 billion |

| Total Corporate M&A Deals | US$191 billion | |

| Total Asset Acquisitions | US$43 billion | |

| Total 2023 M&A | US$234 billion | |

(Data Sources: EIA, Evaluate Energy, Corporate SEC Filings)

Chevron isn’t the only acquirer that is running into challenges closing its deal. In early April, Chesapeake and Southwestern Energy said that the closing date of their proposed deal could be pushed back to the second half of the year after the Federal Trade Commission (FTC) sought increased scrutiny over the oil and gas M&A.

In the same vein, Oxy delayed its acquisition of CrownRock, pushing its timeline back to Q3 of this year. “Our teams are working constructively with the FTC, and we anticipate that the transaction will close in the third quarter of this year,” said Occidental Petroleum (Oxy) Chief Financial Officer Sunil Mathew on the company’s Q1 2024 earnings call. “As a reminder, Oxy will benefit from CrownRock’s activity between the transaction’s January 1st, 2024, effective date and close, subject to customary purchase price adjustments. Concurrent with the CrownRock acquisition, we announced a US$4.5 billion to US$6 billion divestiture program to be completed within 18 months of the transaction’s close. The high-quality assets within our portfolio have garnered much interest, and our teams have commenced the early stages of the divestiture process.”

Later in the call, Oxy CEO Vicki Hollub decided not to provide an update on the production or other metrics related to CrownRock but expressed confidence that the deal would close sometime in the third quarter.

Mammoth Midstream Moves

It’s worth mentioning that the US$234 billion in 2023 M&A figure provided by the EIA only includes E&P deals, not midstream or downstream. The midstream industry, in particular, featured multiple high value shakeups. The largest midstream deal of 2023 was the merger of Magellan Midstream Partners LP with Oneok Inc., which was announced in May 2023 and completed in September 2023. The US$18.8 billion merger created one of the largest oil and natural gas pipeline companies in North America.

In September 2023, Enbridge announced the US$14 billion acquisition of three natural gas utilities from Dominion Energy (Dominion). The utilities are the East Ohio Gas Company (East Ohio), Questar Gas, and the Public Service Company of North Carolina. The deal is Enbridge’s largest since it merged with Spectra Energy for US$28 billion in 2016.

On March 7, Enbridge completed its acquisition of East Ohio. The gas utility serves more than 1.2 million customers and includes more than 22,000 miles (35,400 km) of transmission, gathering, and distribution pipelines, underground storage, and interconnections to multiple interstate pipelines and large natural gas producers.

What’s Next For The Industry

According to EIA data, ExxonMobil’s acquisition of Pioneer Natural Resources would give the combined company 7% of total US production, while Chevron and Hess would hold 6% of total US production. The wave of consolidation is concentrating a higher percentage of production among fewer players. However, many of these players have strict medium- and long-term environmental targets.

It remains to be seen how long the majors will follow a kind of “one step forward, two steps back” approach to the energy transition. For the time being, the largest producers are not shying away from ramping production. Chevron, for example, increased US production by a whopping 35% in Q1 2024 compared to Q1 2023. The uptick was driven by added production from PDC Energy, but worldwide production still increased by 12%.

The share price remains the yard stick by which corporations will make their decisions. A few years ago, Wall Street was critiquing producers from overly investing in fossil fuels and was pushing diversification into renewables. Today, renewable energy equity valuations are at multi-year lows while the investment community praises the margins and cash flows available to producers at current oil prices.

M&A activity is likely to slow from here, but we could see a push toward maximizing fossil fuel production in the near-term. At the same time, many producers have been earmarking sizeable expenditures into low-carbon fuels and carbon capture and storage. The energy transition drum is beating on, just to the tune of fuels that work within the oil and gas industry rather than solutions like photovoltaic solar and wind that fall outside of it.

The favorable response to higher production and consolidation is a boon for the oil and gas industry. It indicates that the investment community has turned positive on the industry, which fosters investment, spurs growth, and can support job creation.

{kind=link}